Overlooked Key Metrics That Affect the Value of Your Vacation Rental Business

Most owners of vacation rental management companies think valuation is determined by one thing: profitability. While your profits are extremely important, they’re the starting point of any conversation with a buyer. If you’re a bit rusty, we cover the mechanics of valuation methods in our article how vacation rental companies are valued. The multiple that is applied to your profits is a function of the quality of your company. There are many factors that separate a smooth, premium exit from a bumpy, discounted one.

You’re likely familiar with some of the more obvious factors that affect a sale — unit churn rate, pacing vs same time last year, and financial hygiene. But there are a handful of sneakier ones that often get overlooked.

Here are some overlooked factors that buyers will scrutinize when they’re underwriting an acquisition, and what you should be tracking now if a sale is on your horizon.

1. Founder Involvement & Key Man Risk

Founder involvement, often called “key man risk”, is the single biggest hidden value driver in any vacation rental management acquisition. Buyers want to know whether the business can operate without the seller, and the answer materially affects what they’re willing to pay.

The concern is valid. If you, as the owner, are the primary point of contact for your homeowners, buyers see a big, bright red flag. When you exit the business, those contracts are at risk. Homeowner churn after a sale is one of the most common ways an acquisition underperforms, and you better believe buyers price that risk into their offer.

A founder who owns homeowner relationships doesn’t just lower the multiple, they often extend the transition period by 12 to 24 months, with earnouts tied to retention. That’s money and freedom you don’t get back.

The other factor of key man risk is operational. If the business depends on you to manage pricing, approve marketing spend, or close new homeowner contracts, buyers know they can’t simply slot in their own leadership and move on. They’ll either discount the offer, structure a longer earnout, or walk away from the deal entirely.

What to do about it: start delegating homeowner relationships now. Build a sales team that can sign new owners without you. Document your SOPs. Hire or promote a general manager who can run the business while you take a step back. The goal isn’t to be absent. It’s to prove the business doesn’t need you. Even modest progress here can meaningfully change how a buyer underwrites your company.

2. Technology Stack

Buyers pay more for businesses running modern, integrated technology, and discount businesses running on outdated or stitched-together systems. Your tech stack is one of the first things a sophisticated buyer will diligence.

The core question is your property management system (PMS). Companies running on Streamline, Track, Guesty, or other modern platforms signal operational sophistication and make a buyer’s integration job manageable. Companies running on outdated or proprietary systems force the buyer to plan a costly, time consuming migration and they’ll either deduct that cost from your purchase price or pass on the deal.

The same logic applies to revenue management. If you’re using Wheelhouse, Pricelabs, Beyond, or a similar dynamic pricing tool, you’re telling a buyer that your revenue isn’t dependent on a single person. If you’re still pricing manually or relying on static seasonal rates, that’s a flag.

Beyond the PMS and rev management, buyers care about how connected your stack is. Is your CRM talking to your PMS? Is your accounting clean and integrated? Can a buyer get a clean data export, or will they spend months reconstructing your numbers? The cleaner the data, the lower the friction in diligence, the higher the offer.

3. Operational Culture & Team Continuity

Culture is the part of a business buyers can’t see on a spreadsheet, but it’s something they’ll assess in diligence conversations and site visits. The reason is simple: an acquisition only works if the “boots on the ground” are reliable, stay through the transition and operate effectively under new ownership.

Buyers look for specific signals. Low turnover in key operational roles tells them the team is stable and engaged. Documented processes tell them the business has institutional knowledge that doesn’t walk out the door with any single person. A clear chain of command tells them the company can absorb new leadership without operational chaos.

The other dimension is cultural fit with the buyer. Strategic acquirers think hard about whether your team will integrate well with theirs, because the cost of cultural misalignment is real: key employees leave in the first 12 months, homeowner relationships get rocky, and the operational synergies the buyer modeled in their thesis evaporate. A strong, well-documented internal culture makes you a more attractive acquisition target because it lowers that integration risk.

4. Inventory Quality & Portfolio Consistency

Not every property in your portfolio is equally valuable to a buyer. Two companies with identical revenue can sell for very different multiples based on the quality and consistency of their inventory.

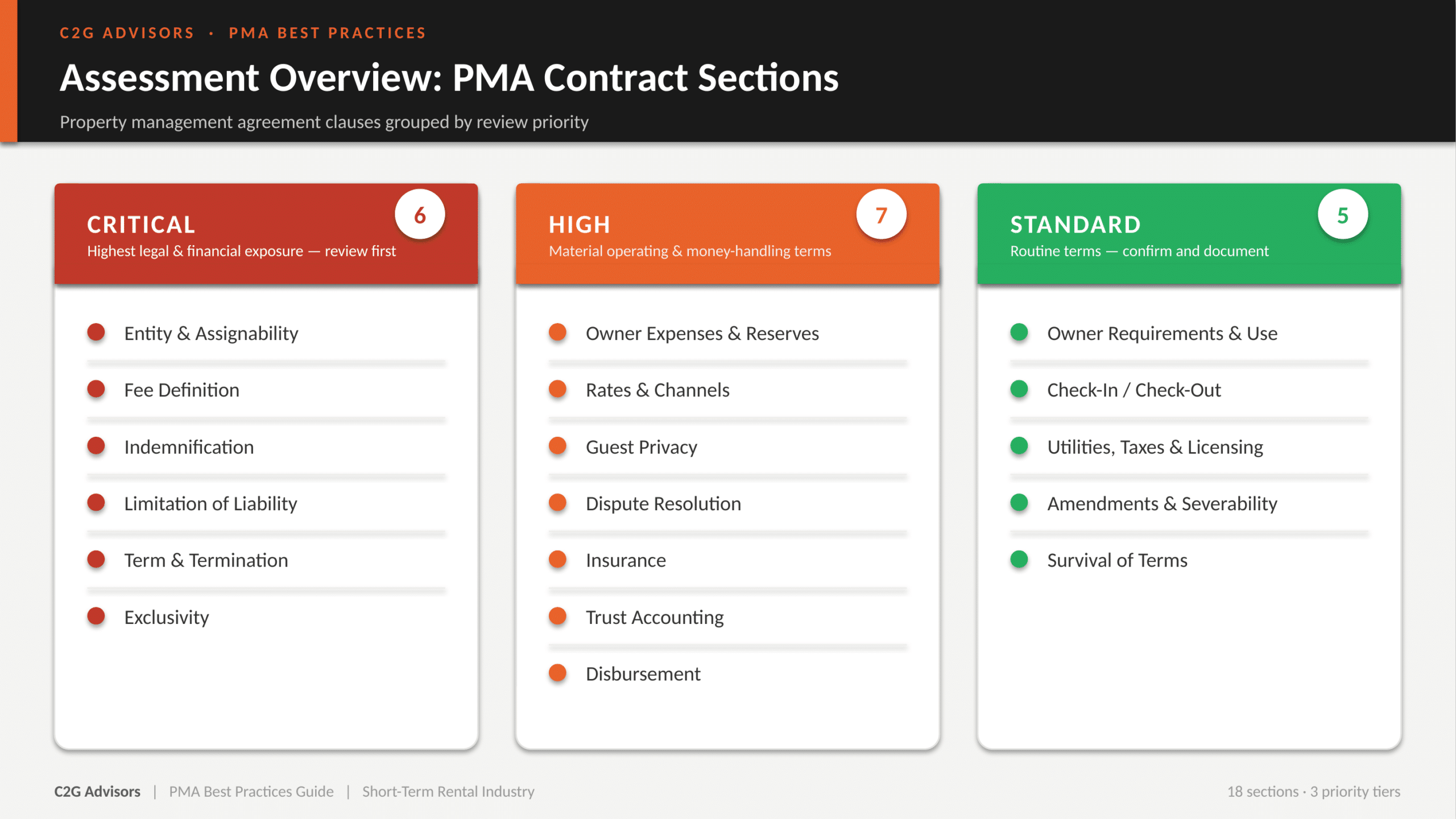

While “quality” does mean premium, well-maintained homes, it also means strong homeowner contracts with favorable terms for the business — strong commission structures, agreements set up to auto-renew, clean cancellation provisions, and more. For a deeper look at the specific contract clauses buyers scrutinize during diligence, see our guide to the 6 critical sections of a short-term rental management agreement.

Revenue concentration risk is the other side of this coin. If 30% of your revenue comes from your top five homes, a buyer could see this as acquiring a fragile business — losing one or two owners post-close materially impacts the financials. The more your revenue is spread across a healthy number of homes, the more durable your business looks on paper.

5. Geographic Density

Where your homes are matters as much as how many you have. Depth in a single market is dramatically more valuable to most buyers than the same number of properties spread across multiple regions.

Here’s why. A buyer who already operates in 30A is going to see immediate operational synergy in acquiring another 30A company. They can share cleaning crews, consolidate local market expertise, leverage existing vendor relationships, and concentrate marketing spend on a region they already know. The acquired homes plug directly into their existing infrastructure. That synergy translates directly to a higher multiple.

Now imagine the opposite. You have 80 homes total, but they’re scattered: 30 in Flagstaff, 30 in Palm Springs, and 20 in a third tertiary market. To a buyer with operations in 30A or the Outer Banks, those properties offer almost no strategic synergy. They’d have to spin up local operations in three different regions to absorb your business — which means it’s not really an acquisition, it’s three new market expansions wrapped in a deal. Most buyers won’t pay much for that, and many won’t pay at all.

The strategic takeaway: if you’re thinking about an exit in the next few years, build deep before you build wide. A 100-home portfolio concentrated in one or two markets is far more valuable than a 150-home portfolio spread across five.

6. Brand Legacy & Domain Authority

“Brand” in this context means two distinct but related things, and buyers care about both. The first is brand recognition in your local market — being the name homeowners and guests think of when they think about your destination. The second is domain authority in the SEO sense — your website’s organic search strength and direct booking volume.

Both matter because they reduce a buyer’s dependence on the OTAs. A business that books 50% of its nights direct, through its own brand and website, is fundamentally more valuable than a business booking 95% through Airbnb and Vrbo. The OTA-dependent business is one algorithm change away from a revenue crisis. The brand-driven business has a moat.

Specifically, buyers will look at your direct booking percentage, your branded search volume (how many people search for your company name each month), your backlink profile, and your organic traffic trends over the past two to three years. If those numbers are strong and growing, it shows up in the offer. If they’re weak or declining, expect a discount.

The good news: this is one of the most measurable parts of your business, and it’s something a sell-side advisor can quantify clearly in a confidential information memorandum (CIM) — turning what feels like a soft asset into a hard data point that justifies a higher multiple.

Frequently Asked Questions

What is key man risk in a vacation rental business?

Key man risk is the degree to which a business depends on a single person — usually the founder or owner — to operate successfully. In vacation rental management, this typically shows up as the owner being the primary point of contact for homeowners, the only person setting strategic pricing, or the sole decision-maker on new owner contracts. High key man risk lowers the valuation multiple because buyers worry the business will lose homeowners or stumble operationally once the seller exits.

Why do buyers care about geographic concentration?

Buyers pay more for portfolios concentrated in one market because they create operational synergy with an existing buyer’s footprint. A buyer with operations in a market can absorb additional homes there using shared cleaning crews, local vendors, regulatory expertise, and marketing infrastructure. Scattered portfolios across multiple unrelated markets force the buyer to spin up new operations in each region, which most strategic buyers won’t pay for. Density beats breadth in most VRM acquisitions.

What technology should a vacation rental company use to maximize value?

Modern, integrated systems signal operational sophistication and make a buyer’s job easier in diligence and post-close integration. The most important component is the property management system — modern platforms are familiar to buyers and reduce migration risk. A revenue management tool signals data-driven pricing rather than founder intuition. Beyond those, buyers value clean integrations between the PMS, CRM, and accounting systems so financial data can be extracted and trusted without months of reconstruction.

How can I increase the value of my vacation rental business before selling?

The highest-leverage moves are the ones that take 12 to 24 months to execute, which is why the best time to start is well before you’re ready to sell. Focus on: reducing key man risk by delegating homeowner relationships and operations; strengthening owner contracts with longer terms and exclusivity; building portfolio density in your strongest markets; investing in direct bookings and brand authority to reduce OTA dependence; and modernizing your tech stack to clean up your data and integration story. A pre-sale valuation can identify which of these levers will move your multiple most.

Start Optimizing Before You’re Ready to Sell

The owners who exit at the top of the multiple range are the ones who started optimizing these metrics 18 to 36 months before going to market. By the time you’re actively in a sale process, most of these levers are out of reach — you can’t undo years of founder dependency or build market density in three months.

If you’re considering an exit in the next one to three years, the right move is to get a valuation now. It tells you what your business is worth today, where the gaps are, and which of these hidden value drivers would give you the most upside if you focused on them between now and the sale. Request a confidential business valuation to find out where your business stands.